I. Context: Rising Interest Rates, More “Conservative” Investors?

Over the past three years, financial markets in the US and Europe have experienced dramatic interest rate fluctuations. Since 2022, the US Federal Reserve has continuously raised interest rates to combat high inflation. By the end of 2024, the federal funds rate had reached 5.25%–5.50%. The European Central Bank followed suit, raising its main refinancing rate to 4.5%.

This round of tightening has ushered investors out of the “zero-interest era.” Meanwhile, the stock market has shown increasingly polarized performance, with growing return gaps between tech stocks and major indexes. As risk appetite declines, more people are reconsidering low-risk, steady-return investment strategies.

Among middle-class families in the US and Europe, a more conservative financial mindset is making a comeback: rather than gambling in the stock market, many prefer to park their funds where they can sleep soundly—Certificates of Deposit (CDs) or Money Market Funds (MMFs).

Are you also considering moving part of your portfolio from stocks to low-risk assets?

II. Term Deposits in 2025: Safe, But Lacking Flexibility?

(1) Current Interest Rate Overview

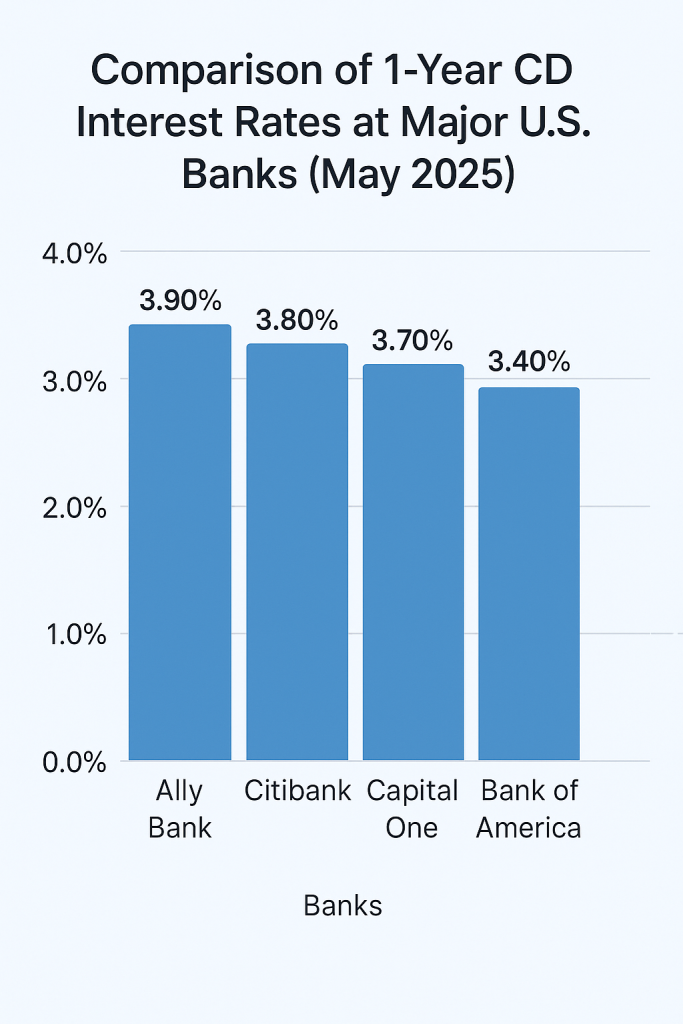

According to Bankrate data from April 2025, most online banks in the US offer 1-year CD rates ranging from 4.80% to 5.25%. Synchrony Bank, for example, offers up to 5.15% APY—significantly higher than traditional banks like Chase or Bank of America, which offer around 3.5%.

In Europe, savers in Germany can earn approximately 3.7% on 1-year deposits. Among the UK’s top 10 banks, term deposit rates generally hover around 4.2%, while France and Italy offer slightly lower rates of about 3%–3.5%.

High-yield online banks like Ally Bank and Marcus are more attractive than traditional institutions, drawing large amounts of liquidity.

(2) Pros of Term Deposits

The most appealing aspect of CDs is government protection. In the US, deposits are insured by the FDIC (Federal Deposit Insurance Corporation) for up to $250,000 (principal + interest). In Europe, similar national deposit insurance mechanisms exist—for example, Germany’s EdB (Entschädigungseinrichtung deutscher Banken).

For those who don’t plan to touch their funds in the short term, CDs offer a way to “lock in” yields and stay insulated from market volatility.

(3) Cons of Term Deposits

The main downside of CDs is poor liquidity: early withdrawals typically incur penalty interest of several months.

Also, locking in rates too early during a rising rate cycle can mean missing out on future gains. More importantly, if inflation stays above 3%, your real returns could be eroded.

III. Money Market Funds in 2025: Higher Returns, But Are They Really Safe?

(1) Current Yield Levels

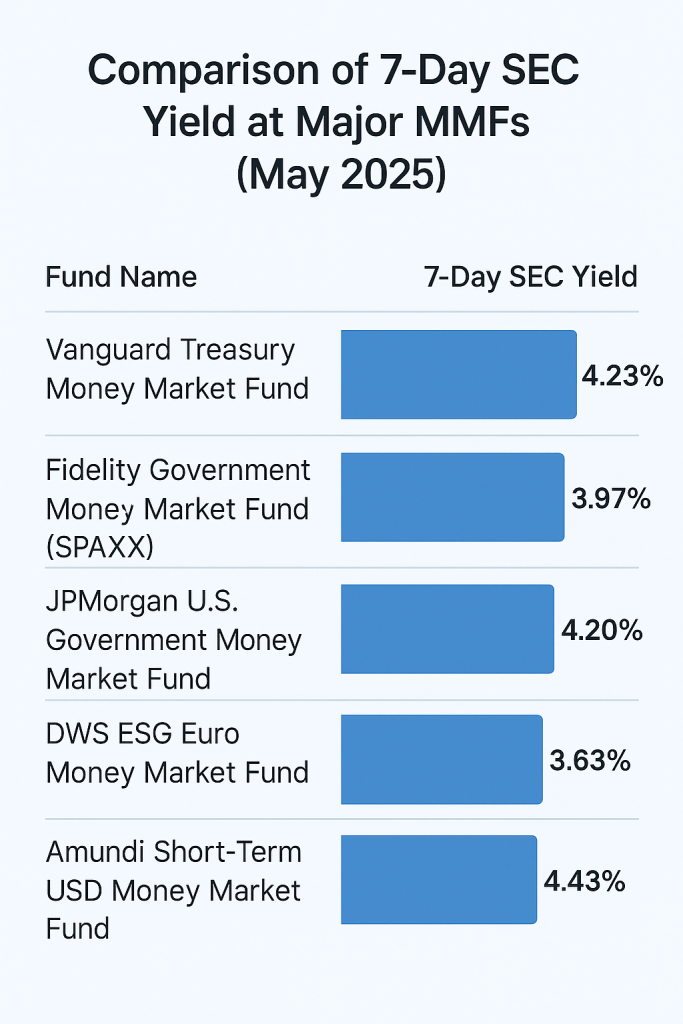

Money Market Funds (MMFs) in the US have seen significantly higher returns in 2025. As of May, Fidelity Money Market Fund had a 7-day yield of 5.03%, and Vanguard Federal Money Market Fund offered 4.87%—both outperforming most CDs.

In Europe, firms like DWS and Amundi offer MMFs with yields around 3.2%–4.0%. Exact returns depend on short-term interest rates and fund fees.

Funds based on short-term government bonds tend to provide stable returns. Institutional MMFs may offer slightly higher yields but usually come with stricter liquidity rules.

(2) Pros of Money Market Funds

The biggest advantage of MMFs is their high liquidity. Most mainstream MMFs allow same-day (T+0) redemptions, making funds immediately accessible—ideal for emergency or short-term capital needs.

Even more crucially, their yields adjust with market interest rates, offering a kind of “automatic adjustment” during rising-rate periods.

(3) Potential Risks

However, MMFs are not FDIC-insured. While the risk is typically very low, extreme events can still pose threats.

For instance, during the 2008 Lehman crisis, the first US MMF to “break the buck” triggered mass redemptions. Though post-2020 reforms have strengthened liquidity safeguards, MMFs still shouldn’t be considered “absolutely safe.”

IV. Real-Life Case Studies: Two Families, Two Choices

Case 1: US Retired Couple Prefers CDs

George and Catherine from Virginia are in their 60s, living on retirement income and medical insurance. They value capital safety and stable interest income.

At the end of 2024, they placed $200,000 into CDs from three banks offering 5% interest rates. They split the funds into 12-month, 18-month, and 24-month terms. This strategy spreads risk and creates a “ladder” so one CD matures every six months.

Case 2: German Freelancer Chooses MMF

Lena, a 35-year-old freelance illustrator in Berlin, has highly variable income. She values liquidity and wants to avoid being “locked in.”

In early 2025, she invested €50,000 in the iShares Euro Government Bond 0–6 Month UCITS ETF. By May, the fund offered an annualized return of about 3.8%, and she could redeem it daily without fees.

Which situation sounds more like your current financial goals?

V. Full Comparison Table: See the Differences at a Glance

| Comparison Dimension | Term Deposits (CDs) | Money Market Funds (MMFs) |

|---|---|---|

| Safety | Extremely high; government-insured | High, but no FDIC coverage |

| Return | Fixed; generally lower than MMFs | Floating; generally higher in 2025 |

| Liquidity | Poor; early withdrawals penalized | Excellent; redeemable any time |

| Minimum Investment | Low; often under $100 | No minimum on most platforms |

| Inflation Protection | Weak; fixed rates lose to inflation | Stronger; adjusts with market rates |

| Risk Source | Virtually none | Rare extreme cases can lead to losses |

| Best For | Older, conservative, stable income | Younger, flexible, middle-class investors |

VI. Which Should You Choose? Tailored Advice by Your Goal

✅ If You Are:

- Looking to lock in rates for over 12 months → Term Deposit

- Needing access to funds at any time with decent returns → Money Market Fund

✅ Based on Your Goal:

- Saving for a house down payment: → MMF (maintains flexibility)

- Child’s college tuition next year: → CD (guarantees capital at a set date)

- Conservative retirement allocation: → Mixed strategy: CD + MMF

Pro Tip: A combined strategy often works better than choosing one. For example, a 6-month CD laddered with MMFs can balance yield and liquidity.

VII. Commonly Overlooked Questions: Have You Considered These?

- Is the CD rate APY or simple interest? Some banks advertise compound APY, others simple—check calculation methods carefully.

- What are the MMF fees? Some platforms hide management fees that silently eat into your returns.

- What does the fund actually invest in? Government-bond MMFs are lowest-risk; commercial paper funds carry more risk. Always read the prospectus.

- Don’t ignore tax implications: In countries like Germany or France, MMF returns may be taxed as capital gains, reducing your net income.

VIII. It’s Not About “Highest Yield,” but “Right Timing, Right Use”

Many people instinctively ask: “MMFs yield more—shouldn’t I just choose them?” But in reality, financial products are not about absolute pros and cons—they’re about fit.

CDs offer predictable peace of mind. MMFs provide more flexibility and upside.

The key questions are:

- When do you need to use the money?

- Can you tolerate fluctuations?

- Do you have an emergency fund?

At the end of the day, a truly smart investor doesn’t chase the highest yield—they choose the product that helps them reach their goal at the right time, in the right way.